Backtesting

Analysis, Anticipation, Success

Analysis, Anticipation, Success

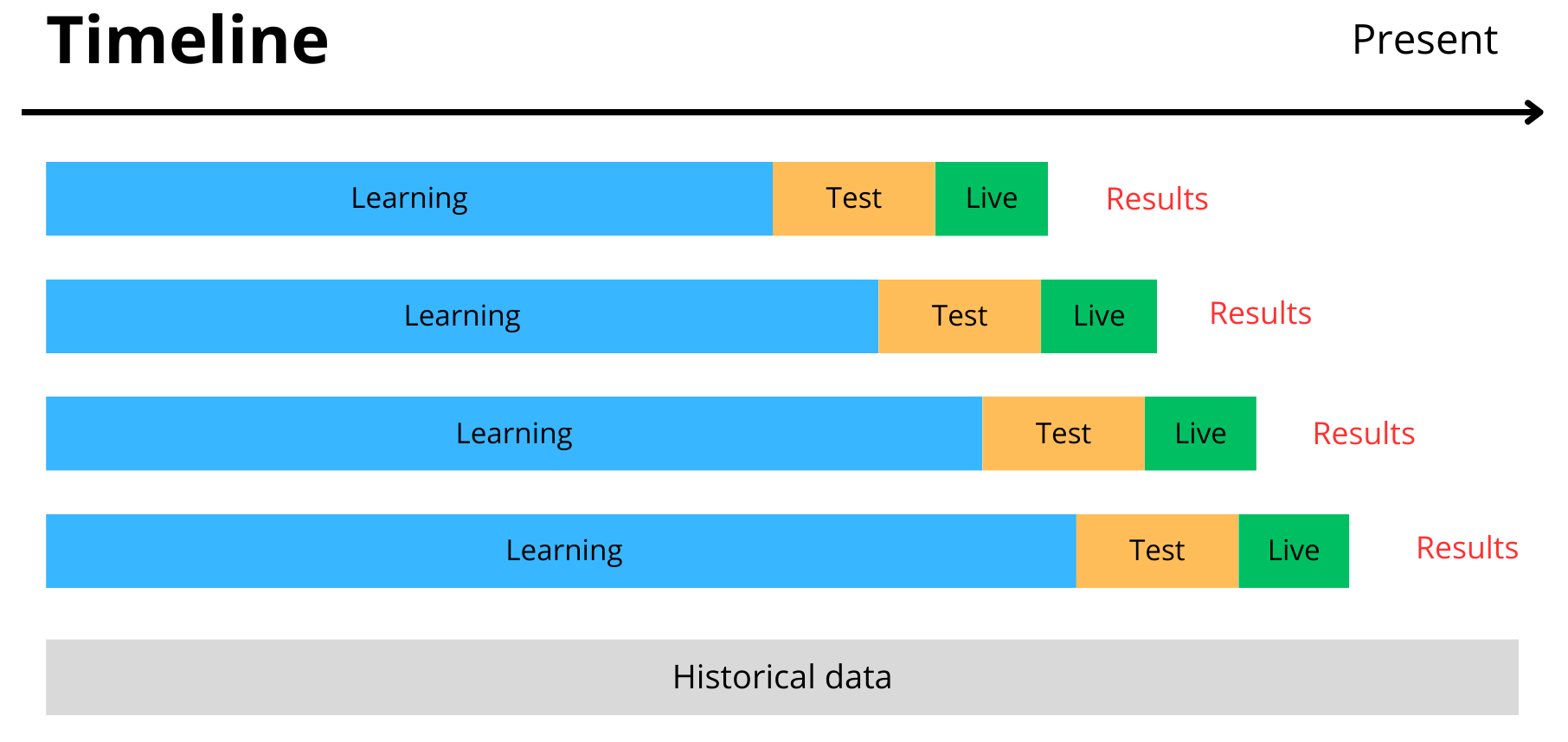

In the context of time series forecasting, backtesting refers to the process of evaluating the accuracy of a forecasting method using existing historical data. The process is typically iterative and repeated across multiple dates present in the historical data. Backtesting is used to estimate the expected future accuracy of a forecasting method, which is useful for assessing which forecasting model should be considered the most precise.

How does our backtesting work ?

The process begins with the selection of a series of data potentially similar in terms of volatility to the upcoming period.This series is then divided into three parts :

Once the results are obtained, we repeat this process every morning to fine-tune the parameters of IaQuantWave to the best possible extent.

During the backtest, we position ourselves at a past date and simulate the process to understand the outcomes.

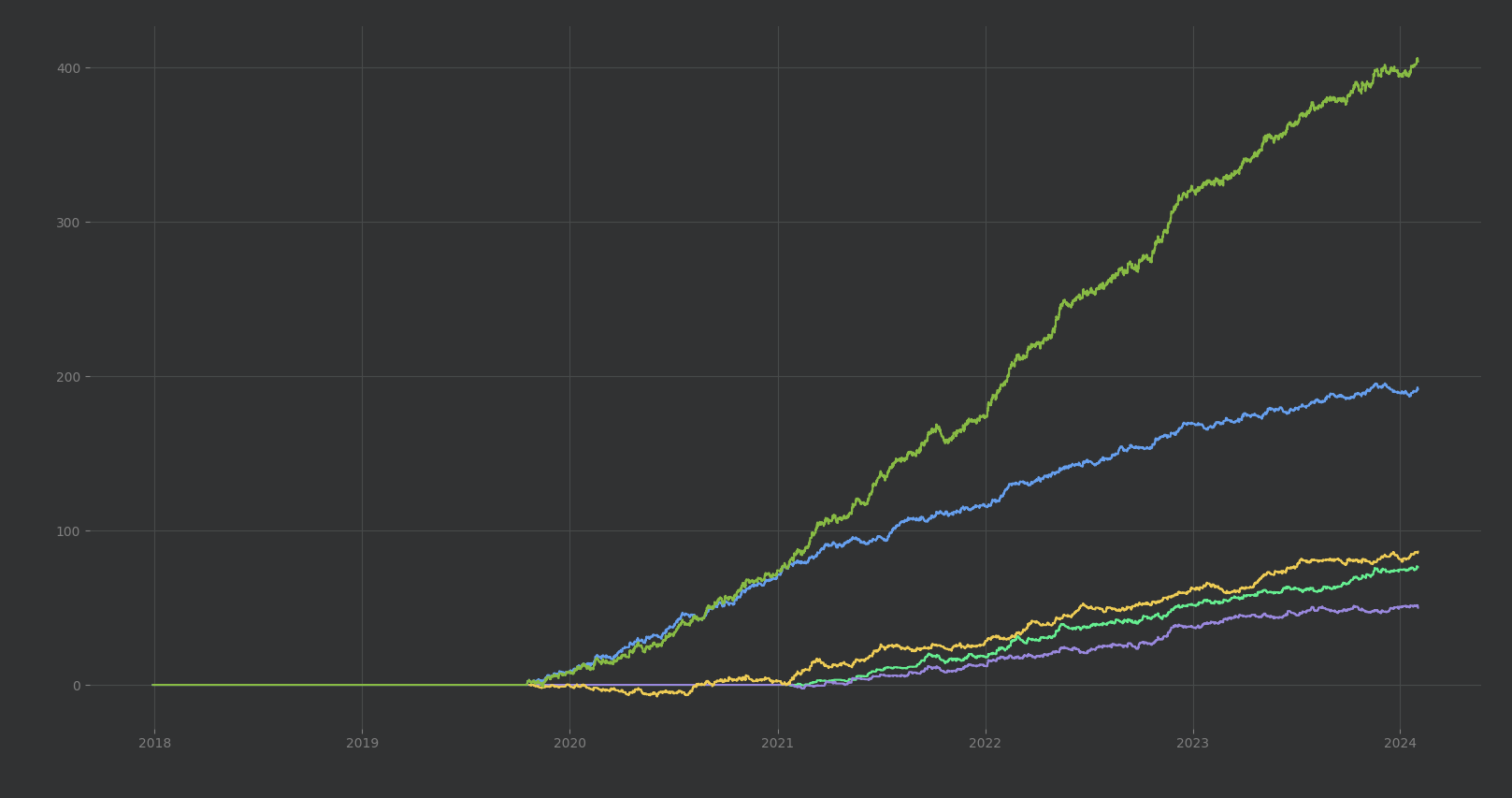

A quick overview of the results from our backtesting.

Every day, the system adapts to the situation and continues its learning process to enhance its performance.